NOTE: this was a past issue of my weekly newsletter, Timeless Gems. Join my free mailing list so you don’t miss out on future issues.

Today’s gem is this 2016 blog post snippet on Chipotle’s store economics and some discussion around organic reinvestment.

Good businesses generate a high ROIC but great businesses reinvest at a high ROIC. There are 2 ways in which a business can reinvest its capital: organic (growth capex) or inorganic (acquisitions). I’ve discussed inorganic growth in a previous post on serial acquirers. So I wanted to discuss organic reinvestment in this post.

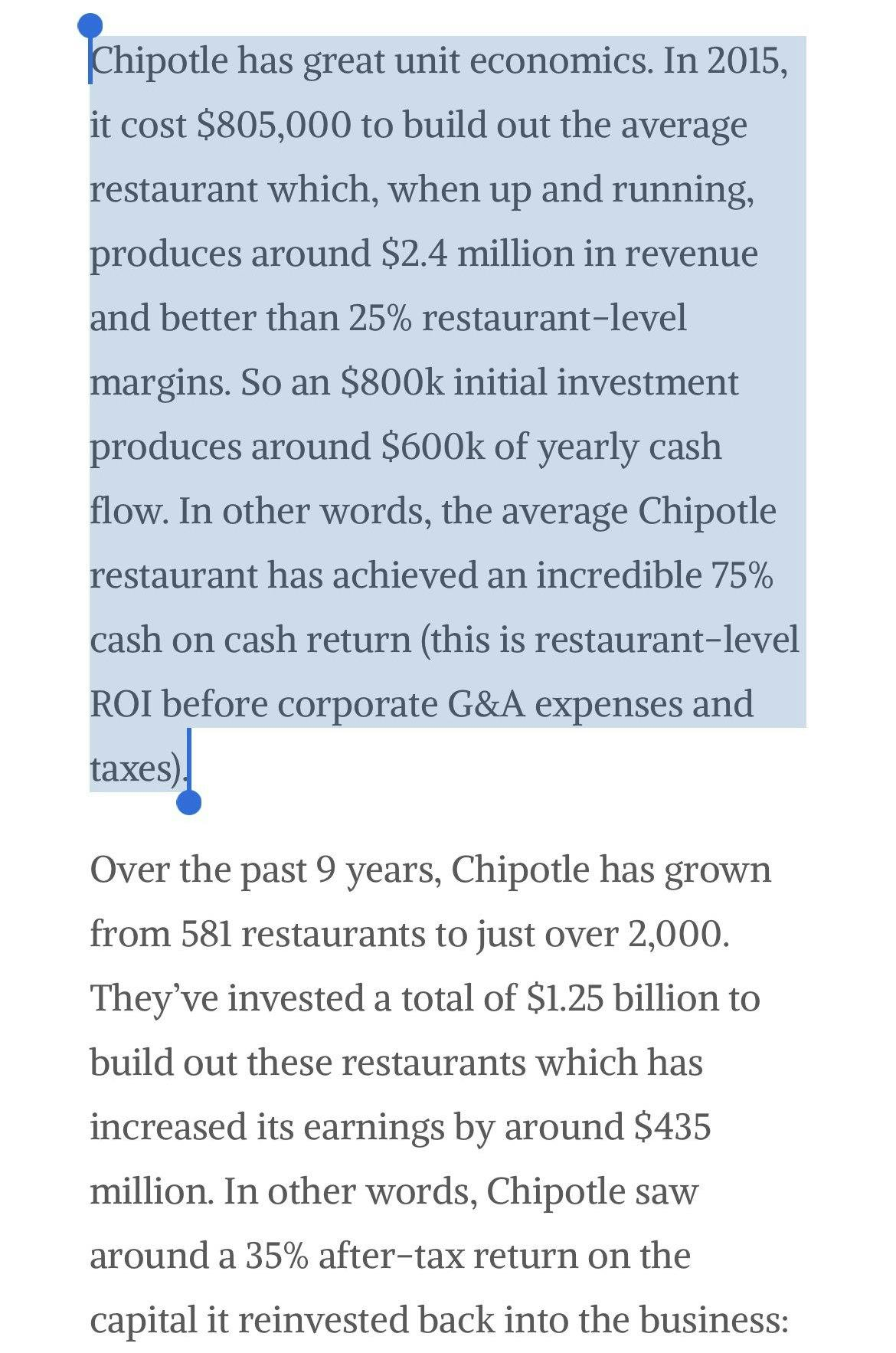

This Chipotle snippet is great because it lays out clearly what the ROIC is on their organic reinvestment. Many growing retailers and location-based businesses operate similarly in terms of organic reinvestment. Spend capital to open a new location, that new location generates a level of earnings – tangible ROIC calculation to justify growth.

At Atlasview, we acquire businesses that aren’t typically location-based (software/services/etc.) and measuring ROIC on organic reinvestment is a bit more difficult. This is why we generally prefer inorganic reinvestment. But there are 2 broad buckets of organic reinvestment we consider:

1) Research & Development

This includes developing new features, functionalities, products, and modules to attract new customers or generate more revenue from existing customers. R&D investment in software is commonly misunderstood by investors, and the lines between growth capex and maintenance capex can be blurred (wrote a post about this before).

ROIC for growth capex R&D ultimately comes down to how costly the development is (driven by difficulty/complexity), and how much customers will pay for it once it’s complete. We prefer to get a level of commitment from existing customers before pulling the trigger (and in some cases, a client might be willing to pay for the entire cost of the new development).

2) Sales & Marketing

Many might view S&M as simply opex, but there is an argument to be made that it could be considered “growth capex”. S&M spending enables you to acquire customer contracts, which is an intangible asset that generates $$.

ROIC for S&M spending boils down to the cost to acquire a new customer (CAC) versus the lifetime of gross profit a new customer generates (LTV). 3.0 is considered to be a great LTV to CAC ratio, but the payback period should also be considered. If you can spend $1 in advertising today and generate $3 within 2 years, that is an incredible ROIC. But if it takes 10 years to generate that $3, you might be better off allocating that $1 elsewhere.

The problem with S&M spend is that the returns diminish quickly as you scale the spending. Not to mention, thanks to Google and algorithmic advertising, the LTV to CAC ratio can compress rapidly in any competitive industry. So the return on incremental S&M investment is likely to produce a far lower return than historical returns.

Payback period

Payback period (how long it takes to make 1x your investment) is an underrated metric. Many investors and operators don’t consider payback period, but I believe it’s the most important metric to consider for organic reinvestment. It will dictate how much capital is required for growth, and how risky the organic growth initiatives are. The longer the payback period, generally, the more capital you need and the riskier the investment is.

Money costs money, so any reinvestment (organic or inorganic) should always be measured and compared against returning capital back to debt and or equity holders.

I took this Chipotle snippet from this 2016 blog post by Saber Capital, it’s a fantastic read.